It differs from the marginal cost because marginal cost includes labor, direct expenses, and variable overheads, whereas differential cost includes both fixed and variable costs. Suppose the decision is whether to drive your carto work every day for a year versus taking the bus for a year. Ifyou bought a second car for commuting, certain costs such asinsurance and an auto license that are fixed costs of owning a carwould be differential costs for this particular decision. Differential cost may be referred to as either incremental cost or decremental cost.

Related Terms:

Differential cost is a technique of decision-making in which the cost between various alternatives is compared and contrasted with choosing between the most competing alternative. It is useful when you want to understand a) Whether to process the product further or not and b) Whether to accept an additional order at a lower current price. Since a differential cost is only used for management decision making, there is no accounting entry for it. There is also no accounting standard that mandates how the cost is to be calculated. Instead, it is simply an analysis concept used to optimize decisions. The telecom operator currently spends $400 on newspaper ads and $100 on maintaining the company’s website every month.

Differential Cost vs. Opportunity Cost

This cost includes all relevant expenses directly connected to each decision, not just the obvious ones. In the case of ABC Company, moving to television ads and social media marketing exposes the company to a broader customer base. If the company earned $10,000 using the current marketing platforms, moving to the more advanced advertising platforms might result in a 40% revenue increase to $14,000. It is advisable to accept the second proposal provided facilities exist for the production of additional numbers of ‘utility’ and to convert them into ‘Ace’.

2: Differential Analysis

- Any price above this minimum selling price represents incremental profit for the company.

- The raw material price and the direct labor cost both make a difference, so both of these costs would be relevant as you looked at your options.

- For instance, a company producing widgets will incur higher costs for materials and labor as it produces more widgets.

- Differential cost is the variation in costs (increase/decrease) between two available opportunities.

- Differential costs are often taken as marginal costs or incremental costs.

Variable costs fluctuate directly with the level of production or business activity. These costs increase as production ramps up and decrease when production slows down. Examples include raw materials, direct labor, and utilities directly tied to manufacturing processes. For instance, a company producing widgets will incur higher costs for materials and labor as it produces more widgets. Understanding variable costs is crucial for businesses because they directly impact the marginal cost of production.

Differential cost refers to the difference between the cost of two alternative decisions. The cost occurs when a business faces several similar options, and a choice must be made by picking one option and dropping the other. When business executives face such situations, they must select the most when does your business need a w viable option by comparing the costs and profits of each option. A bed & breakfast inn owner uses differential analysis to decide whether to renovate a first-floor guest bedroom or to convert that space to a gift shop. A summary of the year’s revenues and costs for the two alternatives follows.

Process of Differential Cost Analysis

(i) Prepare a schedule showing the total differential costs and increments in revenue. The alternative which shows the highest difference between the incremental revenue and the differential cost is the one considered to be the best choice. Differential cost is the change in cost that results from adoption of an alternative course of action. It can be determined simply by subtracting cost of one alternative from cost of another alternative or from the cost at one level of activity, the cost at another level of activity. Differential cost is the variation in costs (increase/decrease) between two available opportunities.

The new regulation renders the machine and the produced plastic bags obsolete, and the company cannot change the government’s decision. The move places the opportunity cost of choosing to stick to the old advertising method at $4,000 ($14,000 – $10,000). The $4,000 is the income that ABC would forego for remaining with the old marketing techniques and failing to adopt the more sophisticated marketing models. Based on this differential analysis, JoannaBennett should perform her tilling service rather than work at thestable. Of course, this analysis considers only cash flows;nonmonetary considerations, such as her love for horses, could swaythe decision. (ii) To continue the present level of output of ‘utility’ but double the production of ‘Ace’.

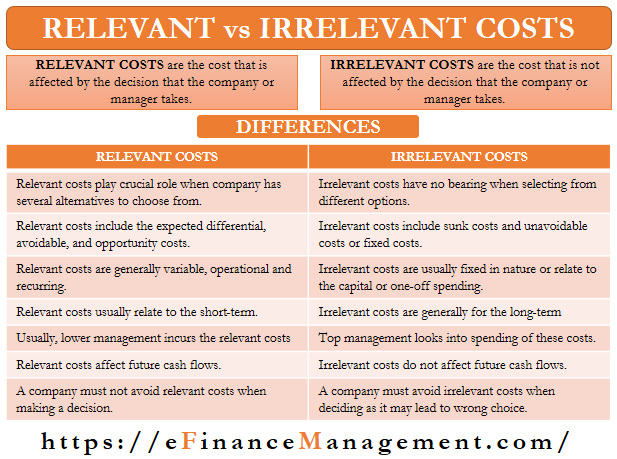

Irrelevant costs, such as sunk costs, should be excluded from the analysis as they do not influence the future outcomes of the decision. This distinction is crucial for maintaining the accuracy and relevance of the analysis. Diving deeper into the fundamentals, differential cost is a crucial concept in accounting. It’s the change in total costs that results from selecting one option over another. Think of it as the financial impact of choosing between two paths.

Differential cost is the difference in total cost between two different choices. Businesses also use differential cost when thinking about adding or cutting a product line. They add up all avoidable costs that would not exist if they stopped offering a product. They have an alternative to increasing the production of up to 900 by reducing the selling price to 28. In the next section, we will look at examples ofdifferential analysis.

However, the decision to accept or reject the alternative depends on the net gain/loss. Understanding differential costs can significantly impact budgeting, forecasting, and pricing strategies. It allows companies to allocate resources more efficiently and improve profitability.

For the company to know if the new selling price is viable, it calculates the differential cost by deducting the cost of the current capacity from the cost of the proposed new capacity. The differential cost is then divided by the increased units of production to determine the minimum selling price. Any price above this minimum selling price represents incremental profit for the company. The company then calculates the estimated revenue by multiplying the expected output at a specific level by the selling price. If change in cost occurs due to change in level of activity, differential cost is referred to as incremental cost in case of increase in output and decremental cost in case of decrease in output. However, in practice, no distinction is made between differential cost and incremental or decremental cost and two terms are used to mean the same thing.